Focus on Exports Should Support Next Leg of Growth For Nitin Spinners Limited

Summary

- Versatile product mix & innovative offerings are expected to provide Nitin Spinners Limited a competitive edge.

- Pent up demand and reduced channel inventory should lend support to sales growth in FY22.

- Export demand should be led by competitive domestic cotton prices and trade tensions between US and China. With recovery in demand, growth should come from volumes and realisations in FY22.

About Nitin Spinners Limited

Established in 1992, Nitin Spinners Limited is being counted among one of leading and renowned manufacturers of cotton yarn, knitted fabrics, greige and finished woven fabrics. The company’s portfolio includes quality products, catering to different end-user applications. Over past 2 decades, the company has evolved into reliable brand for its clients across India and abroad. Innovation capabilities and manufacturing capacity enables the company to meet varied customer needs. The company has worked upon its global presence through exporting top-notch textile products across India, and 50+ countries globally. This company is located in Bhilwara and is connected to all major cities of India and it has proximity to raw material sources and accessibility to modern shipping ports. The company has emerged as one of country’s largest producers of 100% cotton yarns and fabrics.

Growth Enablers of Nitin Spinners Limited

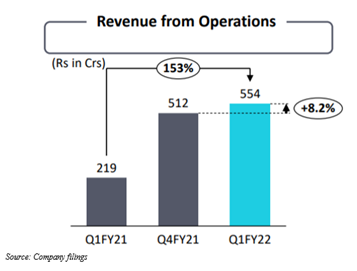

- Higher Exports Supported in 1Q22: In 1Q22, the company saw strong growth in revenues and net profit, with focus maintained on value added products and increase of sustainable fibers such as organic cotton, recycled fibers etc. As a result of lockdown in all major markets, the company saw some disturbances in domestic dispatches. Increased exports took care of these disturbances, with exports contributing 76% to total revenue in comparison to 59% in 4Q21. Out of total yarn revenue, exports made up 88%. The company initiated debottlenecking process and additional 7,296 spindles and other balancing equipment should be operational in 2Q22. This should see addition of ~4% of production capacity.

- Competitive Offerings Should Provide an Edge: The company has state-of -art manufacturing facilities and cost-efficient operations which should continue to lend support. It saw higher productivity and efficient utilization because of investments in R&D and technology. Proper and efficient execution of large projects should result in savings in capital cost and quicker utilization of assets. Domestic manufacturing plants of the company are located in cotton growing belt, which should give logistics and cost advantages. It has strong international presence and long-term relationships with its customers. Plans are there to maintain growth in revenue through optimizing capacity utilisation and it should continue to bring value-added products. The company should continue to target and explore new markets across geographies. Nitin Spinners Limited plans to benefit from various steps taken by government. It plans to capitalize on growth opportunities resulting due to government’s PLI scheme.

- Operating Model Should Lead to Better Financial Numbers: The company’s ability to reprocess waste and using it as an input result in some additional savings of raw material. Not only this, captive solar power and generators supports the company in reducing power cost and ensuring consistent supply of power. Developing of value-added products stems from focused endeavors and strong R&D.

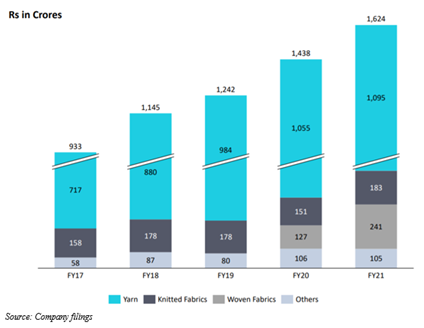

- Addition of New Products in FY20: Revenue from operations during FY20 was INR1,438.06 crores against INR1,242.51 crores in FY19, exhibiting 15.74% increase. Revenue of Yarn saw an increase of 7.14% during FY20 from INR984.19 crores to INR1,054.51 crores. Revenue from yarn made up 73.33% of total sales. Revenue of fabric increased from INR178.06 crores in FY19 to INR277.84 crores during FY20, exhibiting 56.04% growth. Fabric revenue made 19.32% of total revenue from operations. Start of commercial production at new unit at Bhanwaria Kalan, Begun led to increased turnover. Nitin Spinners Limited added new products like blended yarn, woven greige and finished fabrics.

- Capitalising on Sectoral Opportunities: COVID-19 induced lockdown resulted workers to migrate back home, which led to labour shortage. Deploying automation in manufacturing plants should help the companies sustain better to manage shortfall in production during difficult times. The companies can consider exploring other categories of product like medical textiles. These include surgical gloves, personal protective masks etc. and other textile items used in healthcare facilities such as hospital bedsheets, mattresses etc. With increased focus of countries on healthcare, medical textiles should see demand growth. Quicker adoption of e-commerce is another area which creates opportunity. Continuous development is supported by higher penetration of smartphones and lower costs of internet. Since Indian population has access to internet, the companies in both B2B and B2C space should be able to build a stronger customer base.

- India Can See Market Share Gain: Buyers plan to replace China, helping India gain market share. Besides, Indian government’s focus on self-reliance should help in increasing internal demand for raw materials which should result in improved ecosystem for industry. Global textile and apparel industry relies on agricultural sector for raw material and this should support Asian countries. In CY19, valuation of global textile market was USD961.5 billion. Segment wise, textile market is being categorised into natural fibres, polyesters, nylon, and others. Natural fibres include cotton, linen, flax etc. Cotton made up majority of market share with 39.5% in CY2019 and its higher acceptance was principally due to its superior quality such as high absorbency, strength, and colour retention. Global apparel and textile sector growth should seek support from higher demand and lower input cost in developing countries.

- Stringent Cost Control Techniques and Higher Exports Supported FY21: Despite worries about ongoing pandemic, the company saw growth in revenues and in net profit in FY21. With firm establishment of blended yarns and finished woven fabrics, the company saw supplying of finished woven fabrics to renowned international and domestic brands. Better realization and higher exports supported 4Q21 revenue, with revenue going up by 34.6% on year-over-year basis. Techniques about cost control resulted in 4Q21 EBITDA shooting up by 91.5% year-over-year. Revenues in FY21 saw a growth of 13% year-over-year, with export turnover crossing INR1,000 crores.

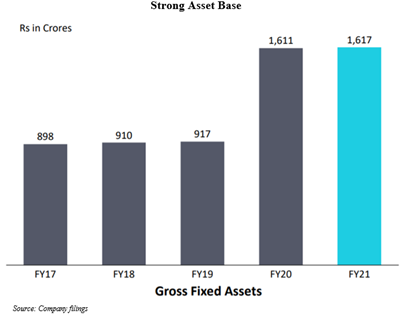

- Strong Asset Base: The company has seen steady expansion of assets portfolio as there were addition of plants to focus on value-added products. Nitin Spinners Limited is working to build strong asset base so that there can be increased contribution of value-added products and international markets can be catered. Return on equity should see some improvement as most of capex is eligible for state investment subsidy.

Absurdly Cheap Valuations Favour Going Long

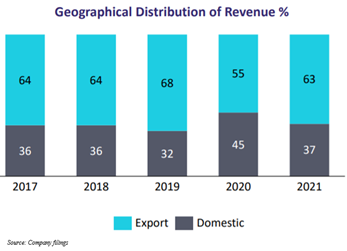

Growth in Nitin Spinners Limited should stem from its strong and developing global presence. In FY21, contribution from exports to revenues has increased. This exhibits that the company has an unwavering focus on international markets. Strong research and development on developing value-added products and systematic processes and its distribution network should be able to result in creation of value for both global and domestic client base. The company exports 63%+ of its production to 60+ countries globally. It has now started focusing on domestic market, as there is higher domestic consumption and per capita spend on clothing.

The company should be able to capitalise on industry dynamics and India is in advantageous position as it has abundant availability of raw materials at international competitive prices which should stem future growth. Additional growth opportunities should come from ban imposed by US on textile items that are made from cotton using prison labour in Xinjiang Autonomous Region in Sept 2020.

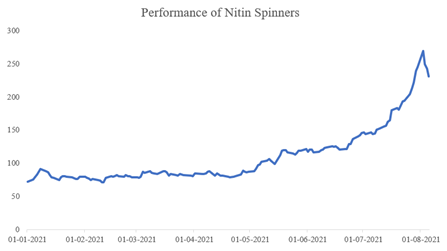

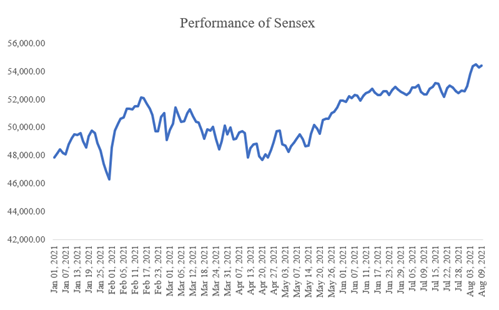

Stock of Nitin Spinners Limited delivered multi-bagger returns in just a few months. Between Jan 1, 2021-Aug 5, 2021, the company’s stock saw a strong run up of ~220.83%. It means an investor who would have invested INR1,00,000 on Jan 1, 2021, would have seen capital grow to INR3,20,833.33. In comparison, Sensex delivered only ~13.84% return between Jan 1, 2021- Aug 5, 2021.

While the company continues to focus on core, it has seen growing contribution of value-added in FY21. Over FY17-FY21, there has been steady increase in yarn sales. In FY20, it added value-added segment of woven fabrics and finished fabrics and the company believes that value-added segments should be able to generate higher profitability.

Solid brand image and healthy research & development capabilities are expected to lend support to the company’s stock price. The company plans to consolidate its existing products and capacities. Latest technologies and continuous investments should continue to support Nitin Spinners Limited in maintaining its market position in cotton yarn and fabric manufacturing. The company’s strong distribution network is another area from where the company seeks to achieve growth. Development in India’s infrastructure, healthy policies for MSMEs and easing labour laws makes entire value chain favourable. Abundant raw material and skilled labour support producers in rationalising costs. End-user industries react in a positive way to favourable demographics and increasing retail outlets. The company trades at ~50.24x of FY20 EPS, which is at a reasonable discount to sectoral average of 56.21x. This level dictates that investors should consider going long on Nitin Spinners Limited.

Exclusivity:

This article is exclusive to investoguru.

Stock Disclosures:

The author has no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

Author Disclosures:

This Article represents the Author's own personal views. The Author did not receive any compensation and do not have any business relationship with any of the companies mentioned in the Article.

share your thoughts

Only registered users can comment. Please register to the website.